Safe Gold Investment: A Buyer’s Guide to Protecting Your Wealth

Gold has captivated investors for millennia-and for good reason. As a hedge against inflation, geopolitical uncertainty, and currency devaluation, gold serves a legitimate role in diversified investment portfolios. But there’s a critical distinction between gold’s value as a portfolio component and the marketing mythology surrounding it. Too many new investors approach gold with the belief that it’s an inherently “safe” investment that will protect them from all economic hardship. That’s not only incorrect; it’s dangerous.

As someone who works in the gold industry and deals with buyers regularly, I’ve seen how misconceptions lead people to make costly mistakes. This guide cuts through the noise and provides evidence-based guidance on how to invest in gold safely-whether you’re exploring your first purchase or managing a significant position.

The truth about gold’s safety

Let’s start with an uncomfortable fact: gold is not inherently safe. The U.S. Commodity Futures Trading Commission (CFTC) is unequivocal on this point:

“The truth is gold and other precious metals are highly volatile and past performance is not a good predictor of future returns.”

Gold prices fluctuate dramatically based on inflation expectations, interest rates, currency strength, and geopolitical events. In 2023, spot gold ranged from $1,810 to $2,085 per ounce-a 15% swing in a single year. That volatility is real, and it affects your returns.

This doesn’t mean gold has no place in your portfolio. It means gold should be treated as a strategic allocation-a diversifier that tends to move opposite to stocks during market stress-not as a wealth protection guarantee. The investors who lose money with gold are typically those who treat it as a standalone hedge or who chase it after prices have already risen significantly.

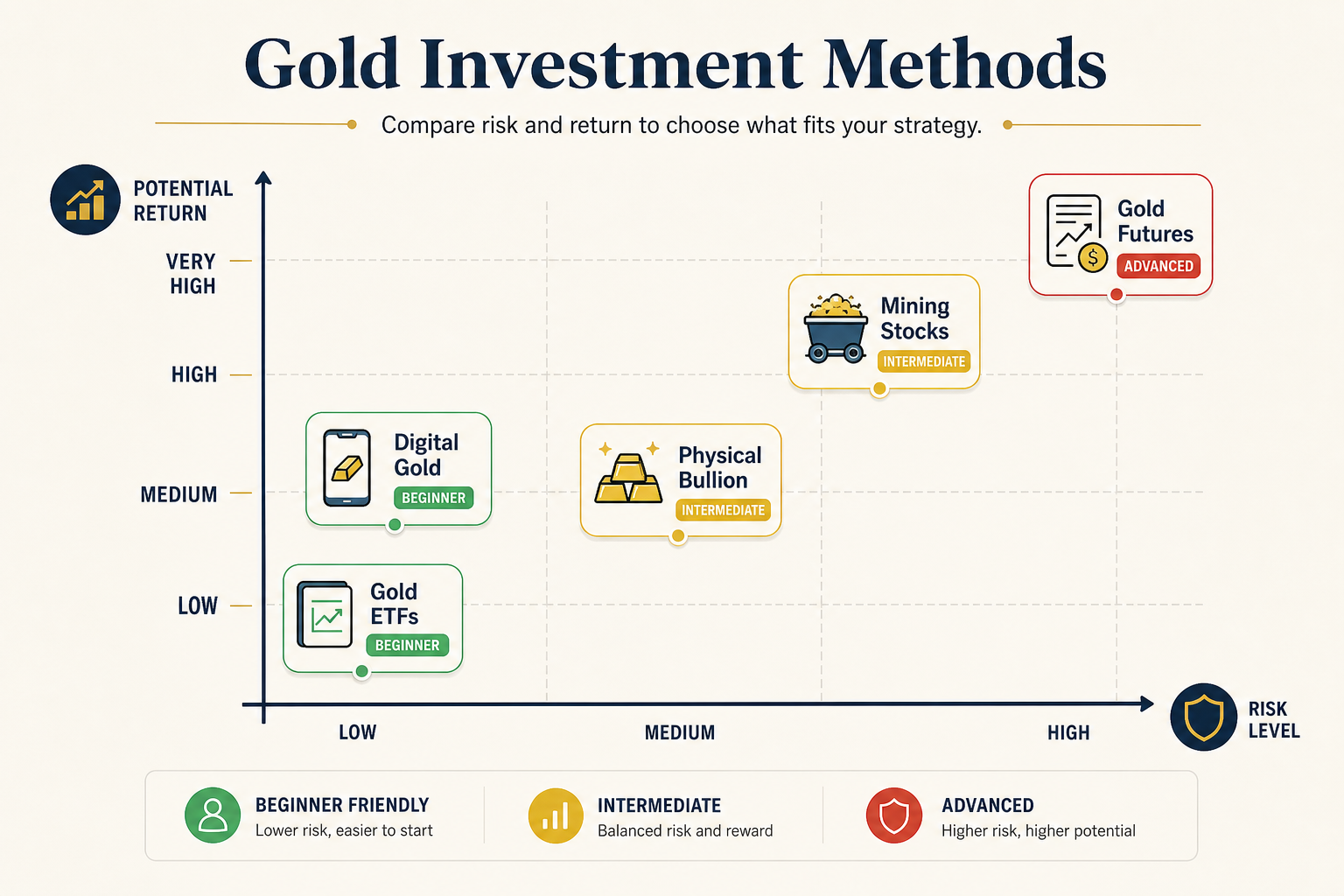

Investment methods: comparing your options

There are multiple ways to gain gold exposure, and each carries different tradeoffs. Your choice depends on your capital, experience level, time commitment, and risk tolerance.

Gold ETFs and mutual funds: the recommended entry point

For most investors, gold ETFs and mutual funds are the best starting point. These securities track the price of gold or invest in gold-mining companies, and they trade like regular stocks through any brokerage account.

Why they’re recommended for beginners:

Extremely low barrier to entry (price of a single share, often under $50)

Minimal annual costs (expense ratios around 0.61%)

No storage, insurance, or handling fees to manage yourself

Easy liquidity-sell whenever you want during market hours

Can be held in standard brokerage accounts, IRAs, and retirement plans

Professional management and regulatory oversight

According to Investopedia, “For the average gold investor, mutual funds and ETFs are generally the easiest and safest way to invest in gold.” This is where most beginners should start.

Physical bullion: direct ownership with real costs

Some investors prefer the tangible security of owning physical gold bars or coins. You control the asset directly, which appeals to those skeptical of financial intermediaries.

Real costs of physical gold ownership:

Cost Element | Typical Range | Impact |

|---|---|---|

Dealer markup | 1-5% above spot price | Immediate loss on purchase |

Insurance (annual) | 0.5-1% of value | Ongoing cost |

Storage (vault) | $100-500+ annually | Reduces returns |

Liquidity discount | 1-3% below spot | Loss when selling |

Total annual cost | 2-9.5% of holdings | Compounded over time |

This is critical: if you buy a gold coin with a 3% markup, pay 0.75% annual storage, and sell with a 2% liquidity discount, you’ve lost 5.75% before the price of gold moves at all. Gold needs to appreciate 5.75% just to break even on these costs alone.

Physical gold makes sense for investors with significant capital ($50,000+), long time horizons, and the financial sophistication to manage storage and insurance arrangements. For most people, ETFs achieve gold exposure with a fraction of the costs.

Gold futures and options: high risk, high leverage

Futures contracts allow you to control large gold positions with minimal margin-but this leverage cuts both ways. A 100-ounce gold futures contract (about $165,000 in notional value) requires only $5,400 in margin. If gold drops just 4%, your entire margin deposit vanishes.

Futures are suitable only for experienced traders who understand derivatives and can afford to lose their entire investment. The CFTC strictly regulates leverage in futures to protect retail investors, but the instrument remains inherently risky.

Gold mining company stocks

Some investors prefer indirect exposure through mining companies. Miners can profit even when gold prices are flat or declining if they hedge effectively or cut costs. Dividends are possible, and you’re diversifying into business execution risk, not just commodity price risk.

The tradeoff: you need to conduct due diligence on individual companies, which requires time and financial analysis skills. A mining company’s stock performance doesn’t always correlate with gold prices.

Digital gold and gold-backed tokens

Emerging platforms now offer fractional ownership of professionally stored gold through digital accounts. These combine the accessibility of ETFs with the tangibility of physical holdings, though regulatory frameworks are still evolving.

Safe allocation: how much gold is too much?

The consensus among financial advisors is remarkably consistent: allocate 5-15% of a diversified portfolio to gold, with 5-10% being a common target.

Why this range?

Gold tends to move opposite to stocks during market corrections, providing diversification benefits

Too little gold (under 5%) has minimal impact; too much creates concentration risk

Age and life stage matter: younger investors might use 5-7%, while those in or near retirement might use 10-15%

Beyond 15%, gold allocation typically exceeds its effective diversification benefit

If you’re building a $100,000 portfolio, this suggests a gold position of $5,000-$15,000. For a $500,000 portfolio, it’s $25,000-$75,000. These are starting points; your specific allocation should reflect your overall financial plan.

Red flags: how to avoid fraud

The gold market attracts sophisticated salespeople and outright fraudsters. Here are the warning signs that should send you elsewhere:

Cold calls and unsolicited offers. Legitimate investment opportunities don’t come from strangers calling your home. This is the #1 indicator of gold investment fraud.

Guaranteed returns. No one can guarantee returns on a volatile commodity. Any seller promising this is either ignorant or dishonest.

Pressure to decide quickly. Real investment decisions benefit from careful analysis. Pressure tactics indicate the seller profits from your haste, not your success.

Excessive dealer markups. A 1-5% markup above spot price is normal for coins; anything beyond 10% is a red flag.

Vague storage or verification arrangements. Your physical gold should be stored in a recognized, insured vault with transparent documentation of your specific holdings. Avoid sellers who offer “allocated” gold without clear proof of your ownership, and never accept unallocated storage (commingled in a vault with others’ holdings without specific assignment to you).

Unverifiable credentials. Check whether the dealer is registered with the Commodity Futures Trading Commission (CFTC) or the National Futures Association (NFA). Legitimate dealers welcome verification; fraudsters avoid it.

Legitimate gold sellers are transparent about pricing, provide clear documentation, explain the costs and risks upfront, and welcome questions. If a seller seems evasive, it’s a clear signal to walk away.

Getting started: a practical approach

If you’ve decided gold belongs in your portfolio, here’s a straightforward process:

Step 1: Define your allocation. Based on your portfolio size and goals, decide how much gold exposure you want (5-10% is a safe starting point for most investors).

Step 2: Choose your investment method. For most people, a gold ETF through a standard brokerage account is the easiest and most cost-effective path.

Step 3: Open a brokerage account if you don’t have one. Firms like Fidelity, Vanguard, and Charles Schwab all offer access to gold ETFs with low fees.

Step 4: Research specific funds. Look for ETFs with low expense ratios (under 0.75%), solid assets under management, and transparent holdings. SPDR Gold Shares (GLD) and iShares Gold Trust (IAU) are widely-held options, though your brokerage likely offers others.

Step 5: Make your initial purchase. Start with your target allocation. You don’t need to time the market perfectly; dollar-cost averaging (investing fixed amounts over time) is a sound approach.

Step 6: Review periodically. Gold shouldn’t require constant attention, but review your allocation annually to ensure it remains in balance with the rest of your portfolio.

The market drivers: understanding gold price movements

Gold prices are influenced by macro factors that savvy investors monitor:

Inflation expectations. Rising inflation expectations push gold higher, as investors seek inflation hedges. The Federal Reserve’s policy signals matter significantly.

Interest rates. Higher real interest rates make non-yielding gold less attractive, pushing prices down. This relationship is inverse but not perfect.

Currency strength. A weaker dollar makes gold cheaper for international buyers, driving demand. Gold is priced in dollars globally, so currency fluctuations matter.

Central bank activity. Major central banks, particularly China and India, actively buy gold reserves. Their actions signal long-term confidence in gold’s role as a reserve asset and can move prices.

Geopolitical risk. War, sanctions, or significant political uncertainty typically drive safe-haven demand for gold, pushing prices higher.

Understanding these drivers helps you avoid panic selling during temporary price dips or chasing momentum after big rallies. Gold works best as a long-term strategic allocation, not a trading vehicle.

Try Crown Ore Group

If you decide to move forward with gold investment-particularly if you’re exploring physical bullion or need guidance on sourcing-Crown Ore Group brings 20+ years of expertise to the table. As a premier international gold and silver mining company, we understand both the producer and buyer perspectives. Our team operates across more than 20 countries and maintains the highest standards of quality and transparency.

Our commitment is simple: Driven by Quality. Built on Trust. Whether you’re sourcing gold for investment, jewelry, or industrial purposes, our engineers and supply chain specialists can guide you through the process, answer your technical questions, and ensure you’re getting genuine, responsibly-sourced material. We provide 365 days of support to our clients because your success is our success.

Reach out to our team at +256 750 488067 or visit our contact page to discuss your needs.

The bottom line

Gold investment isn’t inherently risky or safe-it’s a tool that works when used properly. Start with a clear understanding of the risks, choose an investment method that matches your situation, and maintain a balanced allocation within a diversified portfolio. For most investors, that means a gold ETF representing 5-10% of holdings.

Avoid the myths. Skip the salespeople with unrealistic promises. Focus instead on the fundamentals: low costs, transparency, and a long-term perspective. Done right, gold can play a stabilizing role in your wealth-building strategy for decades to come.